Try all of the on-demand periods from the Clever Safety Summit right here.

It’s been lower than 18 months since we printed our final MAD (Machine Studying, Synthetic Intelligence and Information) panorama, and there have been dramatic developments in that point.

After we left, the info world was booming within the wake of the big Snowflake IPO with an entire ecosystem of startups organizing round it. Since then, in fact, public markets crashed, a recessionary economic system appeared and VC funding dried up. An entire era of information/AI startups has needed to adapt to a brand new actuality.

In the meantime, the previous few months have seen the unmistakable and exponential acceleration of generative AI, with arguably the formation of a brand new mini-bubble. Past technological progress, AI appears to have gone mainstream with a broad group of non-technical individuals around the globe now attending to expertise its energy firsthand.

The rise of information, ML and AI has been one of the elementary developments in our era. Its significance goes properly past the purely technical, with a deep affect on society, politics, geopolitics and ethics. But it’s a sophisticated, technical, quickly evolving world that may be complicated even for practitioners within the area. There’s a jungle of acronyms, applied sciences, merchandise and corporations on the market that’s arduous to maintain a observe of, not to mention grasp.

Occasion

Clever Safety Summit On-Demand

Be taught the essential function of AI & ML in cybersecurity and trade particular case research. Watch on-demand periods in the present day.

The annual MAD panorama is an try at making sense of this vibrant area. Its normal philosophy has been to open supply work that we’d do anyway and begin a dialog with the neighborhood.

So, right here we’re once more in 2023. That is our ninth annual panorama and “state of the union” of the info and AI ecosystem. Listed here are the prior variations: 2012, 2014, 2016, 2017, 2018, 2019 (Half I and Half II), 2020 and 2021. Because the 2021 model was launched late within the yr, I skipped 2022 to give attention to releasing a brand new model within the first quarter of 2023, which seems like a extra pure publishing time for an annual effort.

This annual state of the union submit is organized into 4 elements:

- Half I: The Panorama (PDF right here, interactive model right here)

- Half II: Market developments: Financings, M&A and IPOs (or lack thereof)

- Half III: Information infrastructure developments

- Half IV: Developments in ML/AI

MAD 2023, half I: The panorama

After a lot analysis and energy, we’re proud to current the 2023 model of the MAD panorama. Once I say “we,” I imply slightly group whose nights shall be haunted for months to return by reminiscences of shifting tiny logos out and in of crowded little containers on a PDF: Katie Mills, Kevin Zhang and Paolo Campos. Immense because of them. And sure, I meant it after I instructed them on the onset, “oh, it’s a light-weight venture, perhaps a day or two, it’ll be enjoyable, please signal right here.”

So, right here it’s (cue in drum roll, smoke machine):

As well as, this yr, for the primary time, we’re leaping head first into what the kids name the “World Extensive Internet,” with a completely interactive model of the MAD Panorama that ought to make it enjoyable to discover the varied classes in each “panorama” and “card” format.

Basic strategy

We’ve made the choice to maintain each information infrastructure and ML/AI on the identical panorama. One might argue that these two worlds are more and more distinct. Nevertheless, we proceed to consider that there’s a vital symbiotic relationship between these areas. Information feeds ML/AI fashions. The excellence between an information engineer and a machine studying engineer is usually fairly fluid. Enterprises must have a stable information infrastructure in place so as earlier than correctly leveraging ML/AI.

The panorama is constructed roughly on the identical construction as each annual panorama since our first model in 2012. The free logic is to observe the stream of information from left to proper – from storing and processing to analyzing to feeding ML/AI fashions and constructing user-facing, AI-driven or data-driven functions.

We proceed to have a separate “open supply” part. It’s at all times been a little bit of an ungainly group as we successfully separate business corporations from the open supply venture they’re typically the primary sponsor of. However equally, we need to seize the fact that for one open supply venture (for instance, Kafka), you’ve got many business corporations and/or distributions (for Kafka – Confluent, Amazon, Aiven, and so forth.). Additionally, some open-source tasks showing within the field aren’t totally business corporations but.

The overwhelming majority of the organizations showing on the MAD panorama are distinctive corporations with a really massive variety of VC-backed startups. A lot of others are merchandise (equivalent to merchandise supplied by cloud distributors) or open supply tasks.

Firm choice

This yr, now we have a complete of 1,416 logos showing on the panorama. For comparability, there have been 139 in our first model in 2012.

Annually we are saying we are able to’t probably match extra corporations on the panorama, and every year, we have to. This comes with the territory of overlaying one of the explosive areas of expertise. This yr, we’ve needed to take a extra editorial, opinionated strategy to deciding which corporations make it to the panorama.

In prior years, we tended to present disproportionate illustration to growth-stage corporations based mostly on funding stage (usually Collection B-C or later) and ARR (when obtainable) along with all the massive incumbents. This yr, notably given the explosion of brand name new areas like generative AI, the place most corporations are 1 or 2 years outdated, we’ve made the editorial resolution to characteristic many extra very younger startups on the panorama.

Disclaimers:

- We’re VCs, so now we have a bias in direction of startups, though hopefully, we’ve achieved a great job overlaying bigger corporations, cloud vendor choices, open supply and the occasional bootstrapped corporations.

- We’re based mostly within the US, so we most likely over-emphasize US startups. We do have sturdy illustration of European and Israeli startups on the MAD panorama. Nevertheless, whereas now we have just a few Chinese language corporations, we most likely under-emphasize the Asian market in addition to Latin America and Africa (which simply had a formidable information/AI startup success with the acquisition of Tunisia-born Instadeep by BioNTech for $650M)

Categorization

One of many more durable elements of the method is categorization, particularly, what to do when an organization’s product providing straddles two or extra areas. It’s turning into a extra salient situation yearly as many startups progressively develop their providing, a development we talk about in “Half III – Information Infrastructure.”

It might be equally untenable to place each startup in a number of containers on this already overcrowded panorama. Due to this fact, our normal strategy has been to categorize an organization based mostly on its core providing, or what it’s largely identified for. Consequently, startups usually seem in just one field, even when they do greater than only one factor.

We make exceptions for the cloud hyperscalers (many AWS, Azure and GCP merchandise throughout the varied containers), in addition to some public corporations (e.g., Datadog) or very massive non-public corporations (e.g., Databricks).

What’s new this yr

Principal adjustments in “Infrastructure”

- We (lastly) killed the Hadoop field to mirror the gradual disappearance of the OG Massive Information expertise – the top of an period! We determined to maintain it one final time within the MAD 2021 panorama to mirror the prevailing footprint. Hadoop is definitely not useless, and elements of the Hadoop ecosystem are nonetheless being actively used. Nevertheless it has declined sufficient that we determined to merge the varied distributors and merchandise supporting Hadoop into Information Lakes (and saved Hadoop and different associated tasks in our open supply class).

- Talking of information lakes, we rebranded that field to “Information Lakes/Lakehouses” to mirror the lakehouse development (which we had mentioned within the 2021 MAD panorama)

- Within the ever-evolving world of databases, we created three new subcategories:

- GPU-accelerated Databases: Used for streaming information and real-time machine studying.

- Vector Databases: Used for unstructured information to energy AI functions, see What’s a Vector Database?

- Database Abstraction: A considerably amorphous time period meant to seize the emergence of a brand new group of serverless databases that summary away loads of the complexity concerned in managing and configuring a database. For extra, right here’s a great overview: 2023 State of Databases for Serverless & Edge.

- We thought of including an “Embedded Database” class with DuckDB for OLAP, KuzuDB for Graph, SQLite for RDBMS and Chroma for search however needed to make arduous decisions given restricted actual property – perhaps subsequent yr.

- We added a “Information Orchestration” field to mirror the rise of a number of business distributors in that area (we already had a “Information Orchestration” field in “Open Supply” in MAD 2021).

- We merged two subcategories, “Information observability” and “Information high quality,” into only one field to mirror the truth that corporations within the area, whereas typically coming from completely different angles, are more and more overlapping – a sign that the class could also be ripe for consolidation.

- We created a brand new “Absolutely Managed” information infrastructure subcategory. This displays the emergence of startups that summary away the complexity of sewing collectively a sequence of information merchandise (see our ideas on the Trendy Information Stack in Half III), saving their prospects time, not simply on the technical entrance, but additionally on contract negotiation, funds, and so forth.

Principal adjustments in “Analytics”

- For now, we killed the “Metrics Retailer” subcategory we had created within the 2021 MAD panorama. The concept was that there was a lacking piece within the fashionable information stack. The necessity for the performance actually stays, but it surely’s unclear whether or not there’s sufficient there for a separate subcategory. Early entrants within the area quickly advanced: Supergrain pivoted, Hint constructed an entire layer of analytics on prime of its metrics retailer, and Remodel was lately acquired by dbt Labs.

- We created a “Buyer Information Platform” field, as this subcategory, lengthy within the making, has been heating up.

- On the threat of being “very 2022”, we created a “Crypto/web3 Analytics” field. We proceed to consider there are alternatives to construct essential corporations within the area.

Principal adjustments in “Machine Studying/Synthetic Intelligence”

- In our 2021 MAD panorama, we had damaged down “MLOps” into a number of subcategories: “Mannequin Constructing,” “Function Shops” and “Deployment and Manufacturing.” On this yr’s MAD, we’ve merged every thing again into one large MLOps field. This displays the fact that many distributors’ choices within the area at the moment are considerably overlapping – one other class that’s ripe for consolidation.

- We nearly created a brand new “LLMOps” class subsequent to MLOps to mirror the emergence of a brand new group of startups centered on the particular infrastructure wants for big language fashions. However the variety of corporations there (no less than that we’re conscious of) continues to be too small and people corporations actually simply acquired began.

- We renamed “Horizontal AI” to “Horizontal AI/AGI” to mirror the emergence of an entire new group of research-oriented outfits, lots of which brazenly state synthetic normal intelligence as their final purpose.

- We created a “Closed Supply Fashions” field to mirror the unmistakable explosion of latest fashions during the last yr, particularly within the area of generative AI. We’ve additionally added a brand new field in “Open Supply” to seize the open supply fashions.

- We added an “Edge AI” class – not a brand new matter, however there appears to be acceleration within the area.

Principal adjustments in “Functions”

- We created a brand new “Functions/Horizontal” class, with subcategories equivalent to code, textual content, picture, video, and so forth. The brand new field captures the explosion of latest generative AI startups over the previous few months. In fact, lots of these corporations are skinny layers on prime of GPT and will or is probably not round within the subsequent few years, however we consider it’s a essentially new and essential class and wished to mirror it on the 2023 MAD panorama. Notice that there are just a few generative AI startups talked about in “Functions/Enterprise” as properly.

- With the intention to make room for this new class:

- We deleted the “Safety” field in “Functions/Enterprise.” We made this editorial resolution as a result of, at this level, nearly each one of many 1000’s of safety startups on the market makes use of ML/AI, and we might commit a complete panorama to them.

- We trimmed down the “Functions/Trade” field. Specifically, as many bigger corporations in areas like finance, well being or industrial have constructed some degree of ML/AI into their product providing, we’ve made the editorial resolution to focus totally on “AI-first” corporations in these areas.

Different noteworthy adjustments

- We added a brand new ESG information subcategory to “Information Sources & APIs” on the backside to mirror its rising (if typically controversial) significance.

- We significantly expanded our “Information Providers” class and rebranded it “Information & AI Consulting” to mirror the rising significance of consulting providers to assist prospects dealing with a posh ecosystem, in addition to the truth that some pure-play consulting retailers are beginning to attain early scale.

MAD 2023, Half II: Financings, M&A and IPOs

“It’s been loopy on the market. Enterprise capital has been deployed at an unprecedented tempo, surging 157% year-on-year globally […]. Ever increased valuations led to the creation of 136 newly-minted unicorns […] and the IPO window has been broad open, with public financings up +687%”

Properly, that was…final yr. Or, extra exactly, 15 months in the past, within the MAD 2021 submit, written just about on the prime of the market, in September 2021.

Since then, in fact, the long-anticipated market flip did happen, pushed by geopolitical shocks and rising inflation. Central banks began growing rates of interest, which sucked the air out of a complete world of over-inflated property, from speculative crypto to tech shares. Public markets tanked, the IPO window shut down, and little by little, the malaise trickled down to personal markets, first on the development stage, then progressively to the enterprise and seed markets.

We’ll speak about this new 2023 actuality within the following order:

- Information/AI corporations within the new recessionary period

- Frozen financing markets

- Generative AI, a brand new financing bubble?

- M&A

MAD corporations dealing with recession

It’s been tough for everybody on the market, and Information/AI corporations actually haven’t been immune.

Capital has gone from ample and low-cost to scarce and costly. Firms of all sizes within the MAD panorama have needed to dramatically shift focus from development in any respect prices to tight management over their bills.

Layoff bulletins have develop into a tragic a part of our every day actuality. widespread tracker Layoffs.fyi, most of the corporations showing on the 2023 MAD panorama have needed to do layoffs, together with, for just a few current examples: Snowplow, Splunk, MariaDB, Confluent, Prisma, Mapbox, Informatica, Pecan AI, Scale AI, Astronomer*, Elastic, UIPath, InfluxData, Domino Information Lab, Collibra, Fivetran, Graphcore, Mode, DataRobot, and plenty of extra (to see the complete checklist, filter by trade, utilizing “information”).

For some time in 2022, we had been in a second of suspended actuality – public markets had been tanking, however underlying firm efficiency was holding sturdy, with many persevering with to develop quick and beating their plans.

Over the previous few months, nevertheless, total market demand for software program merchandise has began to regulate to the brand new actuality. The recessionary surroundings has been enterprise-led thus far, with shopper demand holding surprisingly sturdy. This has not helped MAD corporations a lot, because the overwhelming majority of corporations on the panorama are B2B distributors. First to chop spending had been scale-ups and different tech corporations, which resulted in lots of Q3 and This fall gross sales misses on the MAD startups that focus on these prospects. Now, World 2000 prospects have adjusted their 2023 budgets as properly.

We at the moment are in a brand new regular, with a vocabulary that may echo recessions previous for some and shall be an entire new muscle to construct for youthful people: accountable development, value management, CFO oversight, lengthy gross sales cycles, pilots, ROI.

That is additionally the massive return of company governance:

Because the tide recedes, many points that had been hidden or deprioritized all of the sudden emerge in full drive. Everyone seems to be compelled to pay much more consideration. VCs on boards are much less busy chasing the following shiny object and extra centered on defending their current portfolio. CEOs are much less continually courted by obsequious potential next-round traders and uncover the sheer issue of operating a startup when the following spherical of capital at a a lot increased valuation doesn’t magically materialize each 6 to 12 months.

The MAD world actually has not been proof against the excesses of the bull market. For instance, scandal emerged at DataRobot after it was revealed that 5 executives had been allowed to promote $32M in inventory as secondaries, forcing the CEO to resign (the corporate was additionally sued for discrimination).

The silver lining for MAD startups is that spending on information, ML and AI nonetheless stays excessive on the CIO’s precedence checklist. This McKinsey research from December 2022 signifies that 63% p.c of respondents say they anticipate their organizations’ funding in AI to extend over the following three years.

Frozen financing markets

In 2022, each private and non-private markets successfully shut down and 2023 is seeking to be a troublesome yr. The market will separate sturdy, sturdy information/AI corporations with sustained development and favorable money stream dynamics from corporations which have largely been buoyed by capital, hungry for returns in a extra speculative surroundings.

Public markets

As a “scorching” class of software program, public MAD corporations had been notably impacted.

We’re overdue for an replace to our MAD Public Firm Index, however total, public information & infrastructure corporations (the closest proxy to our MAD corporations) noticed a 51% drawdown in comparison with the 19% decline for S&P 500 in 2022. Many of those corporations traded at important premiums in 2021 in a low-interest surroundings. They might very properly be oversold at present costs.

- Snowflake was an $89.67B market cap firm on the time of our final MAD and went on to succeed in a excessive of $122.94B in November 2021. It’s at the moment buying and selling at a $49.55B market cap on the time of writing.

- Palantir was a $49.49B market cap firm on the time of our final MAD however traded at $69.89 at its peak in January 2021. It’s at the moment buying and selling at a $19.14B market cap on the time of writing.

- Datadog was a $42.60B market cap firm on the time of our final MAD and went on to succeed in a excessive of $61.33B in November 2021. It’s at the moment buying and selling at a $25.40B market cap on the time of writing.

- MongoDB was a $30.68B market firm on the time of our final MAD and went on to succeed in a excessive of $39.03B in November 2021. It’s at the moment buying and selling at a $14.77B market cap on the time of writing.

The late 2020 and 2021 IPO cohorts fared even worse:

- UiPath (2021 IPO) reached a peak of $40.53B in Could 2021 and at the moment trades at $9.04B on the time of writing.

- Confluent (2021 IPO) reached a peak of $24.37B in November 2021 and at the moment trades at $7.94B on the time of writing.

- C3 AI (2021 IPO) reached a peak of $14.05B in February 2021 and at the moment trades at $2.76B on the time of writing.

- Couchbase (2021 IPO) reached a peak of $2.18B in Could 2021 and at the moment trades at $0.74B on the time of writing.

As to the small group of “deep tech” corporations from our 2021 MAD panorama that went public, it was merely decimated. For instance, inside autonomous trucking, corporations like TuSimple (which did a conventional IPO), Embark Applied sciences (SPAC), and Aurora Innovation (SPAC) are all buying and selling close to (and even beneath!) fairness raised within the non-public markets.

Given market situations, the IPO window has been shut, with little visibility on when it’d re-open. General IPO proceeds have fallen 94% from 2021, whereas IPO quantity sank 78% in 2022.

Curiously, two of the very uncommon 2022 IPOs had been MAD corporations:

- Mobileye, a world chief in self-driving applied sciences, went public in October 2022 at a $16.7B valuation. It has greater than doubled its valuation since and at the moment trades at market cap of $36.17B. Intel had acquired the Israeli firm for over $15B in 2018 and had initially hoped for a $50B valuation in order that IPO was thought of disappointing on the time. Nevertheless, as a result of it went out on the proper worth, Mobileye is popping out to be a uncommon vibrant spot in an in any other case very bleak IPO panorama.

- MariaDB, an open supply relational database, went public in December 2022 by way of SPAC. It noticed its inventory drop 40% on its first day of buying and selling and now trades at a market cap of $194M (lower than the entire of what it had raised in non-public markets earlier than going public).

It’s unclear when the IPO window could open once more. There’s actually great pent-up demand from quite a lot of unicorn-type non-public corporations and their traders, however the broader monetary markets might want to achieve readability round macro situations (rates of interest, inflation, geopolitical issues) first.

Standard knowledge is that when IPOs develop into a chance once more, the most important non-public corporations might want to exit first to open the market.

Databricks is actually one such candidate for the broad tech market and shall be much more impactful for the MAD class. Like many non-public corporations, Databricks raised at excessive valuations, most lately at $38B in its Collection H in August 2021 – a excessive bar given present multiples, though its ARR is now properly over $1B. Whereas the corporate is reportedly beefing up its methods and processes forward of a possible itemizing, CEO Ali Ghodsi expressed in quite a few events feeling no specific urgency in going public.

Different aspiring IPO candidates on our Rising MAD Index (additionally due for an replace however nonetheless directionally appropriate) will most likely have to attend for his or her flip.

Personal markets

In non-public markets, this was the yr of the Nice VC Pullback.

Funding dramatically slowed down. In 2022, startups raised an mixture of ~$238B, a drop of 31% in comparison with 2021. The expansion market, particularly, successfully died.

Personal secondary brokers skilled a burst of exercise as many shareholders tried to exit their place in startups perceived as overvalued, together with many corporations from the MAD panorama (ThoughtSpot, Databricks, Sourcegraph, Airtable, D2iQ, Chainalysis, H20.AI, Scale AI, Dataminr, and so forth.).

The VC pullback got here with a collection of market adjustments which will depart corporations orphaned on the time they want probably the most assist. Crossover funds, which had a very sturdy urge for food for information/AI startups, have largely exited non-public markets, specializing in cheaper shopping for alternatives in public markets. Inside VC corporations, numerous GPs have or shall be shifting on, and a few solo GPs is probably not in a position (or keen) to boost one other fund.

On the time of writing, the enterprise market continues to be at a state of standstill.

Many information/AI startups, maybe much more so than their friends, raised at aggressive valuations within the scorching market of the final couple of years. For information infrastructure startups with sturdy founders, it was fairly frequent to boost a $20M Collection A on $80M-$100M pre-money valuation, which frequently meant a a number of on subsequent yr ARR of 100x or extra.

The issue, in fact, is that the perfect public corporations, equivalent to Snowflake, Cloudflare or Datadog, commerce at 12x to 18x of subsequent yr’s revenues (these numbers are up, reflecting a current rally on the time of writing).

Startups, due to this fact, have an incredible quantity of rising to do to get anyplace close to their most up-to-date valuations or face important down rounds (or worse, no spherical in any respect). Sadly, this development must occur within the context of slower buyer demand.

Many startups proper now are sitting on stable quantities of money and don’t should face their second of reckoning by going again to the financing market simply but, however that point will inevitably occur except they develop into cash-flow optimistic.

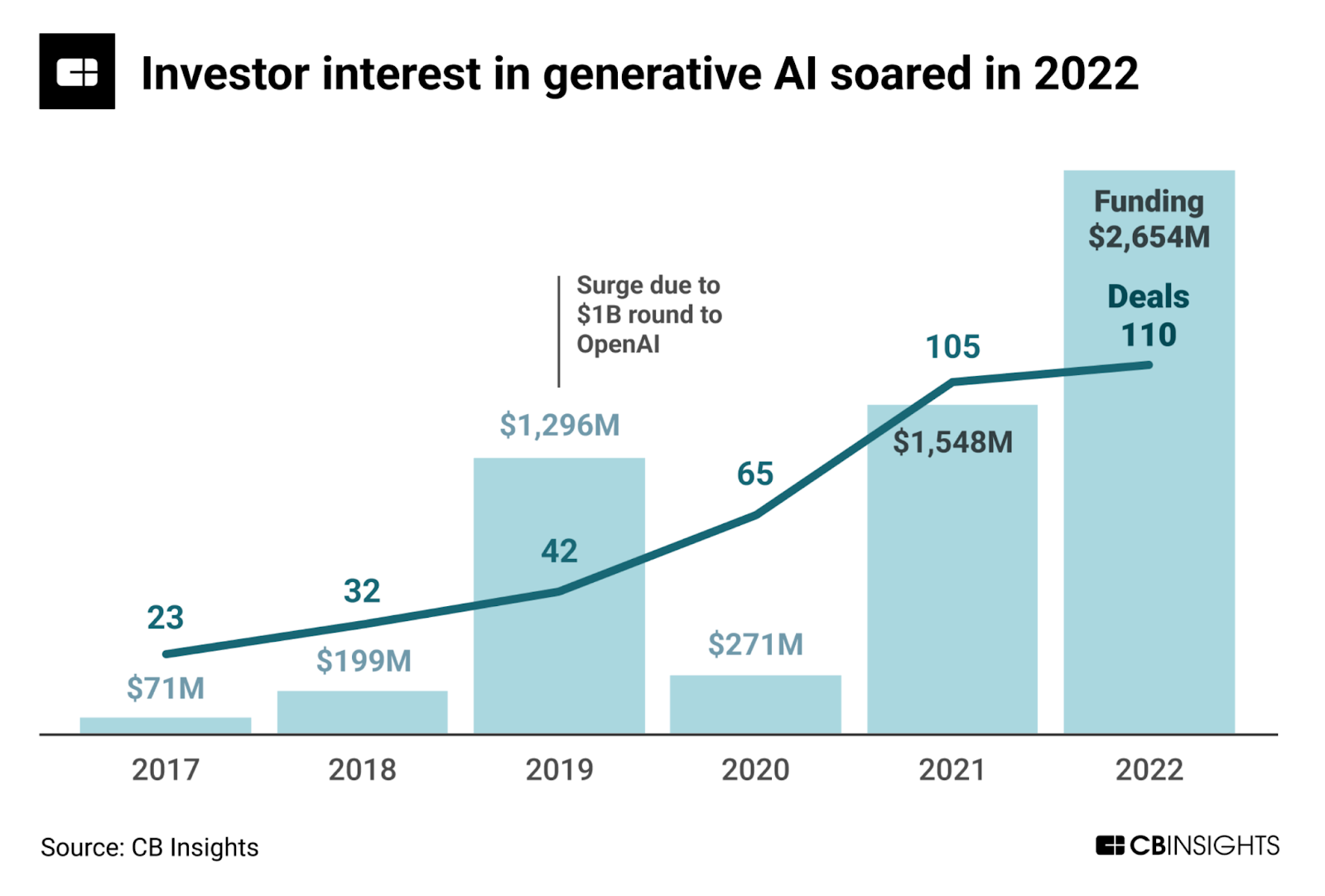

Generative AI: A brand new financing bubble?

Generative AI (see Half IV) has been the one very apparent exception to the final market doom-and-gloom, a vibrant mild not simply within the information/AI world, however in the whole tech panorama.

Significantly because the fortunes of web3/crypto began to show, AI grew to become the recent new factor as soon as once more – not the primary time these two areas have traded locations within the hype cycle:

As a result of generative AI is perceived as a possible “once-every-15-years” sort of platform shift within the expertise trade, VCs aggressively began pouring cash into the area, notably into founders that got here out of analysis labs like OpenAI, Deepmind, Google Mind, and Fb AI Analysis, with a number of AGI-type corporations elevating $100M+ of their first rounds of financing.

Generative AI is displaying some indicators of being a mini-bubble already. As there are comparatively few “property” obtainable available on the market relative to investor curiosity, valuation is usually no object in terms of profitable the deal. The market is displaying indicators of quickly adjusting provide to demand, nevertheless, as numerous generative AI startups are created impulsively.

Noteworthy financings in generative AI

OpenAI obtained a $10B funding from Microsoft in January 2023; Runway ML, an AI-powered video modifying platform, raised a $50M Collection C at a $500M valuation in December 2022; ImagenAI, an AI-powered picture modifying and post-production automation startup, raised $30 million in December 2022; Descript, and AI-powered media modifying app, raised $50M in its Collection C in November 2022; Mem, an AI-powered note-taking app, raised $23.5M in its Collection A in November 2022; Jasper AI, an AI-powered copywriter, raised $125M at a $1.5B valuation in October 2022; Stability AI, the generative AI firm behind Steady Diffusion, raised $101M at $1B valuation in October 2022; You, an AI-powered search engine, raised $25M in its Collection A financings; Hugging Face, a repository of open supply machine studying fashions, raised $100M in its Collection C at a $1B valuation in Could 2022; Inflection AI, AGI startup, raised $225M in its first spherical of fairness financing in Could 2022; Anthropic, an AI analysis agency, raised $580M in its Collection B (traders together with from SBF and Caroline Ellison!) in April 2022; Cohere, an NLP platform, raised $125M in its Collection B in February 2022.

Count on much more of this. Cohere is reportedly in talks to boost lots of of thousands and thousands of {dollars} in a funding spherical that would worth the startup at greater than $6 billion

M&A

2022 was a troublesome yr for acquisitions, punctuated by the failed $40B acquisition of ARM by Nvidia (which might have affected the aggressive panorama of every thing from cell to AI in information facilities). The drawdown within the public markets, particularly tech shares, made acquisitions with any inventory element costlier in comparison with 2021. Late-stage startups with sturdy steadiness sheets, alternatively, usually favored lowering burn as an alternative of creating splashy acquisitions. General, startup exit values fell by over 90% yr over yr to $71.4B from $753.2B in 2021.

That stated, there have been a number of massive acquisitions and quite a lot of (presumably) small tuck-in acquisitions, a harbinger of issues to return in 2023, as we anticipate many extra of these within the yr forward (we talk about consolidation in Half III on Information Infrastructure).

Personal fairness corporations could play an outsized function on this new surroundings, whether or not on the purchase or promote facet. Qlik simply introduced its intent to purchase Talend. That is notable as a result of each corporations are owned by Thoma Bravo, who presumably performed marriage dealer. Progress additionally simply accomplished its acquisition of MarkLogic, a NoSQL database supplier MarkLogic for $355M. MarkLogic, rumored to have revenues “round $100M”, was owned by non-public fairness agency Vector Capital Administration.

MAD 2023, Half III: Information infrastructure again to actuality

Within the hyper-frothy surroundings of 2019-2021, the world of information infrastructure (nee Massive Information) was one of many hottest areas for each founders and VCs.

It was dizzying and enjoyable on the identical time, and maybe slightly bizarre to see a lot market enthusiasm for merchandise and corporations which are finally very technical in nature.

Regardless, because the market has cooled down, that second is over. Whereas good corporations will proceed to be created in any market cycle, and “scorching” market segments will proceed to pop up, the bar has actually escalated dramatically when it comes to differentiation and high quality for any new information infrastructure startup to get actual curiosity from potential prospects and traders.

Right here is our tackle a few of the key developments within the information infra market in 2023. The primary couple developments are increased degree and ought to be fascinating to everybody, the others are extra within the weeds:

- Brace for affect: bundling and consolidation

- The Trendy Information Stack below strain

- The top of ETL?

- Reverse ETL vs CDP

- Information mesh, merchandise, contracts: coping with organizational complexity

- [Convergence]

- Bonus: What affect will AI have on information and analytics?

Brace for affect: Bundling and consolidation

If there’s one factor the MAD panorama makes apparent yr after yr, it’s that the info/AI market is extremely crowded. Lately, the info infrastructure market was very a lot in “let a thousand flowers bloom” mode.

The Snowflake IPO (the most important software program IPO ever) acted as a catalyst for this whole ecosystem. Founders began actually lots of of corporations, and VCs fortunately funded them (once more, and once more, and once more) inside just a few months. New classes (e.g., reverse ETL, metrics shops, information observability) appeared and have become instantly crowded with quite a lot of hopefuls.

On the client facet, discerning consumers of expertise, typically present in scale-ups or public tech corporations, had been keen to experiment and take a look at the brand new factor with little oversight from the CFO workplace. This resulted in lots of instruments being tried and bought in parallel.

Now, the music has stopped.

On the client facet, consumers of expertise are below increasing finances strain and CFO management. Whereas information/AI will stay a precedence for a lot of, even throughout a recessionary interval, they’ve too many instruments as it’s, they usually’re being requested to do extra with much less. Additionally they have fewer sources to engineer something. They’re much less more likely to be experimental or work with immature instruments and unproven startups. They’re extra more likely to decide established distributors that supply tightly built-in suites of merchandise, stuff that “simply works.”

This leaves the market with too many information infrastructure corporations doing too many overlapping issues.

Specifically, there’s an ocean of “single-feature” information infrastructure (or MLOps) startups (maybe too harsh a time period, as they’re simply at an early stage) which are going to wrestle to fulfill this new bar. These corporations are usually younger (1-4 years in existence), and as a consequence of restricted time on earth, their product continues to be largely a single characteristic, though each firm hopes to develop right into a platform; they’ve some good prospects however not a powerful product-market-fit simply but.

This class of corporations has an uphill battle in entrance of them and an incredible quantity of rising to do in a context the place consumers are going to be weary and VC money is scarce.

Count on the start of a Darwinian interval forward. The most effective (or luckiest, or greatest funded) of these corporations will discover a strategy to develop, develop from a single characteristic to a platform (say, from information high quality to a full information observability platform), and deepen their buyer relationships.

Others shall be a part of an inevitable wave of consolidation, both as a tuck-in acquisition for an even bigger platform or as a startup-on-startup non-public mixture. These transactions shall be small, and none of them will produce the form of returns founders and traders had been hoping for. (we aren’t ruling out the potential of multi-billion greenback mega offers within the subsequent 12-18 months, however these will most probably require the acquirers to see the sunshine on the finish of the tunnel when it comes to the recessionary market).

Nonetheless, consolidation shall be higher than merely going out of enterprise. Chapter, an inevitable a part of the startup world, shall be rather more frequent than in the previous few years, as corporations can not increase their subsequent spherical or discover a house.

On the prime of the market, the bigger gamers have already been in full product enlargement mode. It’s been the cloud hyperscaler’s technique all alongside to maintain including merchandise to their platform. Now Snowflake and Databricks, the rivals in a titanic shock to develop into the default platform for all issues information and AI (see the 2021 MAD panorama), are doing the identical.

Databricks appears to be on a mission to launch a product in nearly each field of the MAD panorama. This product enlargement has been achieved nearly completely organically, with a really small variety of tuck-in acquisitions alongside the way in which – Datajoy and Cortex Labs in 2022. Snowflake has additionally been releasing options at a fast tempo. It has develop into extra acquisitive as properly. It introduced three acquisitions within the first couple of months of 2023 already.

Confluent, the general public firm constructed on prime of the open-source streaming venture Kafka, can be making fascinating strikes by increasing to Flink, a highly regarded streaming processing engine. It simply acquired Immerok. This was a fast acquisition, as Immerok was based in Could 2022 by a workforce of Flink committees and PMC members, funded with $17M in October and purchased in January 2023.

Some barely smaller however nonetheless unicorn-type startups are additionally beginning to develop aggressively, beginning to encroach on different’s territories in an try and develop right into a broader platform.

For instance, transformation chief dbt Labs first introduced a product enlargement into the adjoining semantic layer space in October 2022. Then, it acquired an rising participant within the area, Remodel (dbt’s weblog submit gives a pleasant overview of the semantic layer and metrics retailer idea) in February 2023.

Some classes in information infrastructure really feel notably ripe for consolidation of some type – the MAD panorama gives a great visible help for this, because the potential for consolidation maps fairly intently with the fullest containers:

ETL and reverse ETL: Over the past three or 4 years, the market has funded a great variety of ETL startups (to maneuver information into the warehouse), in addition to a separate group of reverse ETL startups (to maneuver information out of the warehouse). It’s unclear what number of startups the market can maintain in both class. Reverse ETL corporations are below strain from completely different angles (see beneath), and it’s attainable that each classes could find yourself merging. ETL firm Airbyte acquired Reverse ETL startup Grouparoo. A number of corporations like Hevo Information place as end-to-end pipelines, delivering each ETL and reverse ETL (with some transformation too), as does information syncing specialist Phase. Might ETL market chief FIvetran purchase or (much less possible) merge with considered one of its Reverse ETL companions like Census or Hightouch?

Information high quality and observability: The market has seen a glut of corporations that every one need to be the “Datadog of information.” What Datadog does for software program (guarantee reliability and decrease utility downtime), these corporations need to do for information – detect, analyze and repair all points with respect to information pipelines. These corporations come on the downside from completely different angles: Some do information high quality (declaratively or by machine studying), others do information lineage, and others do information reliability. Information orchestration corporations additionally play within the area. A lot of these corporations have wonderful founders, are backed by premier VCs and have constructed high quality merchandise. Nevertheless, they’re all converging in the identical route in a context the place demand for information observability continues to be comparatively nascent.

Information catalogs: As information turns into extra complicated and widespread inside the enterprise, there’s a want for an organized stock of all information property. Enter information catalogs, which ideally additionally present search, discovery and information administration capabilities. Whereas there’s a clear want for the performance, there are additionally many gamers within the class, with sensible founders and powerful VC backing, and right here as properly, it’s unclear what number of the market can maintain. It is usually unclear whether or not information catalogs could be separate entities outdoors of broader information governance platforms long run.

MLOps: Whereas MLOps sits within the ML/AI part of the MAD panorama, additionally it is infrastructure and it’s more likely to expertise a few of the identical circumstances because the above. Like the opposite classes, MLOps performs a vital function within the total stack, and it’s propelled by the rising significance of ML/AI within the enterprise. Nevertheless, there’s a lot of corporations within the class, most of that are well-funded however early on the income entrance. They began from completely different locations (mannequin constructing, characteristic shops, deployment, transparency, and so forth.), however as they attempt to go from single characteristic to a broader platform, they’re on a collision course with one another. Additionally, most of the present MLOps corporations have primarily centered on promoting to scale-ups and tech corporations. As they go upmarket, they could begin bumping into the enterprise AI platforms which have been promoting to World 2000 corporations for some time, like Dataiku, Datarobot, H2O, in addition to the cloud hyperscalers.

The trendy information stack below strain

An indicator of the previous few years has been the rise of the “Trendy Information Stack” (MDS). Half structure, half de facto advertising alliance amongst distributors, the MDS is a collection of contemporary, cloud-based instruments to gather, retailer, remodel and analyze information. On the middle of it, there’s the cloud information warehouse (Snowflake, and so forth.). Earlier than the info warehouse, there are numerous instruments (Fivetran, Matillion, Airbyte, Meltano, and so forth.) to extract information from their unique sources and dump it into the info warehouse. On the warehouse degree, there are different instruments to rework information, the “T” in what was referred to as ETL (extract remodel load) and has been reversed to ELT (right here, dbt Labs reigns largely supreme). After the info warehouse, there are different instruments to research the info (that’s the world of BI, for enterprise intelligence) or extract the remodeled information and plug it again into SaaS functions (a course of referred to as “reverse ETL”).

Up till lately, the MDS was a enjoyable however little world. As Snowflake’s fortunes saved rising, so did the whole ecosystem round it. Now, the world has modified. As value management turns into paramount, some could query the strategy that’s on the coronary heart of the trendy information stack: Dump all of your information someplace (an information lake, lakehouse or warehouse) and determine what to do with it later, which seems to be costly and never at all times that helpful.

Now the MDS is below strain. In a world of value management and rationalization, it’s nearly too apparent a goal. It’s complicated (as prospects must sew every thing collectively and cope with a number of distributors). It’s costly (as each vendor needs their margin and in addition since you want an in-house workforce of information engineers to make all of it work). And it’s arguably elitist (as these are probably the most bleeding-edge, best-in-breed instruments, requiring prospects to be subtle each technically and when it comes to use instances), serving the wants of the few.

What occurs when MDS corporations cease being pleasant and begin competing with each other for smaller buyer budgets?

As an apart, the complexity of the MDS has given rise to a brand new class of distributors that “package deal” numerous merchandise below one totally managed platform (as talked about above, a brand new field within the 2023 MAD that includes corporations like Y42 or Mozart Information). The underlying distributors are a few of the standard suspects in MDS, however most of these platforms summary away each the enterprise complexity of managing a number of distributors and the technical complexity of sewing collectively the varied options.

The top of ETL?

As a twist on the above, there’s a parallel dialogue in information circles as as to whether ETL ought to even be a part of information infrastructure going ahead. ETL, even with fashionable instruments, is a painful, costly and time-consuming a part of information engineering.

At its Re:Invent convention final November, Amazon requested, “What if we might remove ETL completely? That might be a world we’d all love. That is our imaginative and prescient, what we’re calling a zero ETL future. And on this future, information integration is now not a handbook effort”, asserting assist for a “zero-ETL” answer that tightly integrates Amazon Aurora with Amazon Redshift. Underneath that integration, inside seconds of transactional information being written into Aurora, the info is accessible in Amazon Redshift.

The advantages of an integration like this are apparent: No must construct and keep complicated information pipelines, no duplicate information storage (which could be costly), and at all times up-to-date.

Now, an integration between two Amazon databases in itself will not be sufficient to result in the top of ETL alone, and there are causes to be skeptical {that a} Zero ETL future would occur quickly.

However then once more, Salesforce and Snowflake additionally introduced a partnership to share buyer information in real-time throughout methods with out shifting or copying information, which falls below the identical normal logic. Earlier than that, Stripe had launched an information pipeline to assist customers sync cost information with Redshift and Snowflake.

The idea of change information seize will not be new, but it surely’s gaining steam. Google already helps change information seize in BigQuery. Azure Synapse does the identical by pre-integrating Azure Information Manufacturing unit. There’s a rising era of startups within the area like Estuary* and Upsolver. It appears that evidently we’re heading in direction of a hybrid future the place analytic platforms will mix in streaming, integration with information stream pipelines and Kafka PubSub feeds.

Reverse ETL vs. CDP

One other somewhat-in-the-weeds however fun-to-watch a part of the panorama has been the stress between Reverse ETL (once more, the method of taking information out of the warehouse and placing it again into SaaS and different functions) and Buyer Information Platforms (merchandise that mixture buyer information from a number of sources, run analytics on them like segmentation, and allow actions like advertising campaigns).

Over the past yr or so, the 2 classes began converging into each other.

Reverse ETL corporations presumably discovered that simply being a pipeline on prime of an information warehouse wasn’t commanding sufficient pockets share from prospects and that they wanted to go additional in offering worth round buyer information. Many Reverse ETL distributors now place themselves as CDP from a advertising standpoint.

In the meantime, CDP distributors discovered that being one other repository the place prospects wanted to repeat large quantities of information was at odds with the final development of centralization of information across the information warehouse (or lake or lakehouse). Due to this fact, CDP distributors began providing integration with the primary information warehouse and lakehouse suppliers. See, for instance, ActionIQ* launching HybridCompute, mParticle launching Warehouse Sync, or Phase introducing Reverse ETL capabilities. As they beef up their very own reverse ETL capabilities, CDP corporations at the moment are beginning to promote to a extra technical viewers of CIO and analytics groups, along with their historic consumers (CMOs).

The place does this depart Reverse ETL corporations? A method they may evolve is to develop into extra deeply built-in with the ETL suppliers, which we mentioned above. One other method could be to additional evolve in direction of turning into a CDP by including analytics and orchestration modules.

Information mesh, merchandise, contracts: Coping with organizational complexity

As nearly any information practitioner is aware of firsthand: success with information is actually a technical and product effort, but it surely additionally very a lot revolves round course of and organizational points.

In lots of organizations, the info stack seems like a mini-version of the MAD panorama. You find yourself with quite a lot of groups engaged on quite a lot of merchandise. So how does all of it work collectively? Who’s accountable for what?

A debate has been raging in information circles about learn how to greatest go about it. There are loads of nuances and loads of discussions with sensible individuals disagree on, properly, nearly any a part of it, however right here’s a fast overview.

We highlighted the information mesh as an rising development within the 2021 MAD panorama and it’s solely been gaining traction since. The information mesh is a distributed, decentralized (not within the crypto sense) strategy to managing information instruments and groups. Notice the way it’s completely different from a information material – a extra technical idea, mainly a single framework to attach all information sources inside the enterprise, no matter the place they’re bodily situated.

The information mesh results in an idea of information merchandise – which might be something from a curated information set to an utility or an API. The essential concept is that every workforce that creates the info product is totally accountable for it (together with high quality, uptime, and so forth.). Enterprise models inside the enterprise then devour the info product on a self-service foundation.

A associated concept is information contracts: “API-like agreements between software program engineers who personal providers and information shoppers that perceive how the enterprise works with the intention to generate well-modeled, high-quality, trusted, real-time information.” There have been all kinds of enjoyable debates in regards to the idea. The essence of the dialogue is whether or not information contracts solely make sense in very massive, very decentralized organizations, versus 90% of smaller corporations.

Bonus: How will AI affect information infrastructure?

With the present explosive progress in AI, right here’s a enjoyable query: Information infrastructure has actually been powering AI, however will AI now affect information infrastructure?

Some information infrastructure suppliers have already been utilizing AI for some time – see, for instance, Anomalo leveraging ML to establish information high quality points within the information warehouse. However with the rise of Giant Language Fashions, there’s a brand new fascinating angle. In the identical method LLMs can create typical programming code, they will additionally generate SQL, the language of information analysts. The concept of enabling non-technical customers to go looking analytical methods will not be new, and numerous suppliers already assist variations of it, see ThoughtSpot, Energy BI or Tableau. Listed here are some good items on the subject: LLM Implications on Analytics (and Analysts!) by Tristan Helpful of dbt Labs and The Rapture and the Reckoning by Benn Stancil of Mode.

MAD 2023, half IV: Developments in ML/AI

The joy! The drama! The motion!

All people is speaking breathlessly about AI impulsively. OpenAI will get a $10B funding. Google is in Code Pink. Sergey is coding once more. Invoice Gates says what’s been occurring in AI within the final 12 months is “each bit as essential because the PC or the web.” Model new startups are popping up (20 generative AI corporations simply within the winter ’23 YC batch). VCs are again to chasing pre-revenue startups at billions of valuation.

So what does all of it imply? Is that this a type of breakthrough moments that solely occur each few a long time? Or simply the logical continuation of labor that has been occurring for a few years? Are we within the early days of a real exponential acceleration? Or on the prime of a type of hype cycles, as many in tech are determined for the following large platform shift after social and cell and the crypto headfake?

The reply to all these questions is… sure.

Let’s dig in:

- AI goes mainstream

- Generative AI turns into a family title

- The inevitable backlash

- [Big progress in reinforcement learning]

- [The emergence of a new AI political economy]

- [Big Tech has a head start over startups]

- [Are we getting closer to AGI?]

AI goes mainstream

It had been a wild experience on the earth of AI all through 2022, however what actually took issues to a fever pitch was, in fact, the general public launch of Open’s AI conversational bot, ChatGPT, on November 30, 2022. ChatGPT, a chatbot with an uncanny capacity to imitate a human conversationalist, rapidly grew to become the fastest-growing product, properly, ever.

For whoever was round then, the expertise of first interacting with ChatGPT was paying homage to the primary time they interacted with Google within the late nineties. Wait, is it actually that good? And that quick? How is that this even attainable? Or the iPhone when it first got here out. Principally, a primary glimpse into what seems like an exponential future.

ChatGPT instantly took over each enterprise assembly, dialog, dinner, and, most of all, each little bit of social media. Screenshots of sensible, amusing and sometimes improper replies by ChatGPT grew to become ubiquitous on Twitter. All of us simply had to chat about ChatGPT.

By January, ChatGPT had reached 100M customers. An entire trade of in a single day consultants emerged on social media, with a endless bombardment of explainer threads coming to the rescue of anybody who had been battling ChatGPT (actually, nobody requested) and impressive TikTokers instructing us the methods of immediate engineering, which means offering the form of enter that may elicit the very best response from ChatGPT.

After being uncovered to a continuous barrage of tweets on the subject, this was the sentiment:

ChatGPT continued to build up feats. It handed the Bar. It handed the US medical licensing examination.

ChatGPT didn’t come out of nowhere. AI circles had been buzzing about GPT-3 since its launch in June 2020, raving a couple of high quality of textual content output that was so excessive that it was troublesome to find out whether or not or not it was written by a human. However GPT-3 was offered as an API focusing on builders, not the broad public.

The discharge of ChatGPT (based mostly on GPT 3.5) feels just like the second AI actually went mainstream within the collective consciousness.

We’re all routinely uncovered to AI prowess in our on a regular basis lives by voice assistants, auto-categorization of pictures, utilizing our faces to unlock our cell telephones, or receiving calls from our banks after an AI system detected attainable monetary fraud. However, past the truth that most individuals don’t notice that AI powers all of these capabilities and extra, arguably, these really feel like one-trick ponies.

With ChatGPT, all of the sudden, you had the expertise of interacting with one thing that felt like an all-encompassing intelligence.

The hype round ChatGPT is not only enjoyable to speak about. It’s very consequential as a result of it has compelled the trade to react aggressively to it, unleashing, amongst different issues, an epic battle for web search.

The exponential acceleration of generative AI

However, in fact, it’s not simply ChatGPT. For anybody who was paying consideration, the previous few months noticed a dizzying succession of groundbreaking bulletins seemingly daily. With AI, you may now create audio, code, photographs, textual content and movies.

What was in some unspecified time in the future referred to as artificial media (a class within the 2021 MAD panorama) grew to become broadly referred to as generative AI: A time period nonetheless so new that it doesn’t have an entry in Wikipedia on the time of writing.

The rise of generative AI has been a number of years within the making. Relying on the way you take a look at it, it traces it roots again to deep studying (which is a number of a long time outdated however dramatically accelerated after 2012) and the arrival of generative Adversarial Networks (GAN) in 2014, led by Ian Goodfellow, below the supervision of his professor and Turing Award recipient, Yoshua Bengio. Its seminal second, nevertheless, got here barely 5 years in the past, with the publication of the transformer (the “T” in GPT) structure in 2017, by Google.

Coupled with fast progress in information infrastructure, highly effective {hardware} and a essentially collaborative, open supply strategy to analysis, the transformer structure gave rise to the Giant Language Mannequin (LLM) phenomenon.

The idea of a language mannequin itself will not be notably new. A language mannequin’s core operate is to foretell the following phrase in a sentence.

Nevertheless, transformers introduced a multimodal dimension to language fashions. There was separate architectures for laptop imaginative and prescient, textual content and audio. With transformers, one normal structure can now gobble up all kinds of information, resulting in an total convergence in AI.

As well as, the massive change has been the flexibility to massively scale these fashions.

OpenAI’s GPT fashions are a taste of transformers that it educated on the Web, beginning in 2018. GPT-3, their third-generation LLM, is without doubt one of the strongest fashions at the moment obtainable. It may be fine-tuned for a variety of duties – language translation, textual content summarization, and extra. GPT-4 is anticipated to be launched someday in 2024 and is rumored to be much more mind-blowing. (ChatGPT relies on GPT 3.5, a variant of GPT-3).

OpenAI additionally performed a driving function in AI picture era. In early 2021, it launched CLIP, an open supply, multimodal, zero-shot mannequin. Given a picture and textual content descriptions, the mannequin can predict probably the most related textual content description for that picture with out optimizing for a selected job.

OpenAI doubled down with DALL-E, an AI system that may create practical photographs and artwork from an outline in pure language. The notably spectacular second model, DALL-E 2, was broadly launched to the general public on the finish of September 2022.

There are already a number of contenders vying to be the very best text-to-image mannequin. Midjourney, entered open beta in July 2022 (it’s at the moment solely accessible by their Discord*). Steady Diffusion, one other spectacular mannequin, was launched in August 2022. It originated by the collaboration of a number of entities, particularly Stability AI, CompVis LMU, and Runway ML. It presents the excellence of being open supply, which DALL-E 2 and Midjourney aren’t.

These developments aren’t even near the exponential acceleration of AI releases that occurred for the reason that center of 2022.

In September 2022, OpenAI launched Whisper, an computerized speech recognition (ASR) system that permits transcription in a number of languages in addition to translation from these languages into English. Additionally in September 2022, MetaAI launched Make-A-Video, an AI system that generates movies from textual content.

In October 2022, CSM (Widespread Sense Machines) launched CommonSim-1, a mannequin to create 3D worlds.

In November 2022, MetaAI launched CICERO, the primary AI to play the technique recreation Diplomacy at a human degree, described as “a step ahead in human-AI interactions with AI that may interact and compete with individuals in gameplay utilizing strategic reasoning and pure language.”

In January 2023, Google Analysis introduced MusicLM, “a mannequin producing high-fidelity music from textual content descriptions equivalent to “a chilled violin melody backed by a distorted guitar riff.”

One other notably fertile space for generative AI has been the creation of code.

In 2021, OpenAI launched Codex, a mannequin that interprets pure language into code. You should utilize codex for duties like “turning feedback into code, rewriting code for effectivity, or finishing your subsequent line in context.” Codex relies on GPT-3 and was additionally educated on 54 million GitHub repositories. In flip, GitHub Copilot makes use of Codex to recommend code proper from the editor.

In flip, Google’s DeepMind launched Alphacode in February 2022 and Salesforce launched CodeGen in March 2022. Huawei launched PanGu-Coder in July 2022.

The inevitable backlash

The exponential acceleration in AI progress over the previous few months has taken most individuals abruptly. It’s a clear case the place expertise is method forward of the place we’re as people when it comes to society, politics, authorized framework and ethics. For all the thrill, it was obtained with horror by some and we’re simply within the early days of determining learn how to deal with this large burst of innovation and its penalties.

ChatGPT was just about instantly banned by some colleges, AI conferences (the irony!) and programmer web sites. Steady Diffusion was misused to create an NSFW porn generator, Unstable Diffusion, later shut down on Kickstarter. There are allegations of exploitation of Kenyan employees concerned within the information labeling course of. Microsoft/GitHub is getting sued for IP violation when coaching Copilot, accused of killing open supply communities. Stability AI is getting sued by Getty for copyright infringement. Midjourney is likely to be subsequent (Meta is partnering with Shutterstock to keep away from this situation). When an A.I.-generated work, “Théâtre d’Opéra Spatial,” took first place within the digital class on the Colorado State Truthful, artists around the globe had been up in arms.

AI and jobs

Lots of people’s response when confronted with the ability of generative AI is that it’s going to kill jobs. The frequent knowledge in years previous was that AI would steadily automate probably the most boring and repetitive jobs. AI would kill artistic jobs final as a result of creativity is probably the most quintessentially human trait. However right here we’re, with generative AI going straight after artistic pursuits.

Artists are studying to co-create with AI. Many are realizing that there’s a unique form of ability concerned. Jason Allen, the creator of Théâtre d’Opéra Spatial, explains that he spent 80 hours and created 900 photographs earlier than attending to the right mixture.

Equally, coders are determining learn how to work alongside Copilot. AI chief, Andrej Karpathy, says Copilot already writes 80% of his code. Early analysis appears to point important enhancements in developer productiveness and happiness. It appears that evidently we’re evolving in direction of a co-working mannequin the place AI fashions work alongside people as “pair programmers” or “pair artists.”

Maybe AI will result in the creation of latest jobs. There’s already a market for promoting high-quality textual content prompts.

AI bias

A severe strike towards generative AI is that it’s biased and probably poisonous. Provided that AI displays its coaching dataset, and contemplating GPT and others had been educated on the extremely biased and poisonous Web, it’s no shock that this could occur.

Early analysis has discovered that picture era fashions, like Steady Diffusion and DALL-E, not solely perpetuate but additionally amplify demographic stereotypes.

On the time of writing, there’s a controversy in conservative circles that ChatGPT is painfully woke.

AI disinformation

One other inevitable query is all of the nefarious issues that may be achieved with such a robust new device. New analysis reveals AI’s capacity to simulate reactions from specific human teams, which might unleash one other degree in data warfare.

Gary Marcus warns us about AI’s Jurassic Park second – how disinformation networks would make the most of ChatGPT, “attacking social media and crafting faux web sites at a quantity now we have by no means seen earlier than.”

AI platforms are shifting promptly to assist battle again, particularly by detecting what was written by a human vs. what was written by an AI. OpenAI simply launched a brand new classifier to try this, which is thrashing the cutting-edge in detecting AI-generated textual content.

Is AI content material simply… boring?

One other strike towards generative AI is that it might be largely underwhelming.

Some commentators fear about an avalanche of uninteresting, formulaic content material meant to assist with web optimization or show shallow experience, not dissimilarly from what content material farms (a la Demand Media) used to do.

As Jack Clark pouts in his OpenAI publication: “Are we constructing these fashions to counterpoint our personal expertise, or will these fashions finally be used to slice and cube up human creativity and repackage and commoditize it? Will these fashions finally implement a form of cultural homogeneity appearing as an anchor ceaselessly caught previously? Or might these fashions play their very own half in a brand new form of sampling and remix tradition for music?”

AI hallucination

Lastly, maybe the most important strike towards generative AI is that it’s typically simply improper.

ChatGPT, particularly, is thought for “hallucinating,” which means making up info whereas conveying them with utter self-confidence in its solutions.

Leaders in AI have been very specific about it, like OpenAI’s CEO Sam Altman right here:

The large corporations are properly conscious of the chance.

MetaAI launched Galactica, a mannequin designed to help scientists, in November 2022 however pulled it after three days. The mannequin generated each convincing scientific content material and convincing (and sometimes racist) content material.

Google saved its LaMBDA mannequin very non-public, obtainable to solely a small group of individuals by AI Take a look at Kitchen, an experimental app. The genius of Microsoft working with OpenAI as an outsourced analysis arm was that OpenAI, as a startup, might take dangers that Microsoft couldn’t. One can assume that Microsoft was nonetheless reeling from the Tay catastrophe in 2016.

Nevertheless, Microsoft was compelled by competitors (or couldn’t resist the temptation) to open Pandora’s field and add GPT to its Bing search engine. That didn’t go in addition to it might have, with Bing threatening customers or declaring their like to them.

Subsequently, Google additionally rushed to market its personal ChatGPT competitor, the apparently named Bard. This didn’t go properly both, and Google misplaced $100B in market capitalization after Bard made factual errors in its first demo.

The enterprise of AI: Massive Tech has a head begin over startups

The query on everybody’s minds in enterprise and startup circles: what’s the enterprise alternative? The current historical past of expertise has seen a serious platform shift each 15 years or so for the previous few a long time: the mainframe, the PC, the web and cell. Many thought crypto and blockchain structure was the following large shift however, at a minimal, the jury is out on that one for now.

Is generative AI that once-every-15-years form of generational alternative that’s about to unleash an enormous new wave of startups (and funding alternatives for VCs)? Let’s look into a few of the key questions.

Will incumbents personal the market?

The success story in Silicon Valley lore goes one thing like this: large incumbent owns a big market however will get entitled and lazy; little startup comes up with a 10x higher expertise; towards the chances and thru nice execution (and considered from the VCs on the board, in fact), little startup hits hyper-growth, turns into large and overtakes the massive incumbent.

The problem in AI is that little startups are dealing with a really particular sort of incumbents – the world’s largest expertise corporations, together with Alphabet/Google, Microsoft, Meta/Fb and Amazon/AWS.

Not solely are these incumbents not “lazy,” however in some ways, they’ve been main the cost in innovation in AI. Google considered itself as an AI firm from the very starting (“Synthetic intelligence could be the last word model of Google… that’s mainly what we work on,” stated Larry Web page in 2000). The corporate produced many key improvements in AI, together with transformers, as talked about, Tensorflow and the Tensor Processing Items (TPU). Meta/Fb We talked about how Transformers got here from Google, however that’s simply one of many many inventions that the corporate has launched through the years. Meta/Fb created PyTorch, one of the essential and used machine studying frameworks. Amazon, Apple, Microsoft, Netflix have all produced groundbreaking work.

Incumbents even have a few of the perfect analysis labs, skilled machine studying engineers, large quantities of information, great processing energy and massive distribution and branding energy.

And at last, AI is more likely to develop into much more of a prime precedence as it’s turning into a serious battleground. As talked about earlier, Google and Microsoft at the moment are engaged in an epic battle in search, with Microsoft viewing GPT as a chance to breathe new life into Bing and Google, contemplating it a probably life-threatening alert.

Meta/Fb has made an enormous wager in a really completely different space – the metaverse. That wager continues to show to be very controversial. In the meantime, it’s sitting on a few of the greatest AI expertise and expertise on the earth. How lengthy till it reverses course and begins doubling or tripling down on AI?

Is AI only a characteristic?

Past Bing, Microsoft rapidly rolled out GPT in Groups. Notion launched NotionAI, a brand new GPT-3-powered writing assistant. Quora launched Poe, its personal AI chatbot. Customer support leaders Intercom and Ada* introduced GPT-powered options.

How rapidly and seemingly simply corporations are rolling out AI-powered options appears to point that AI goes to be in every single place quickly. In prior platform shifts, a giant a part of the story was that each firm on the market adopted the brand new platform: Companies grew to become internet-enabled, everybody constructed a cell app, and so forth.

We don’t anticipate something completely different to occur right here. We’ve lengthy argued in prior posts that the success of information and AI applied sciences is that they ultimately will develop into ubiquitous and disappear within the background. It’s the ransom of success for enabling applied sciences to develop into invisible.

What are the alternatives for startups?

Nevertheless, as historical past has proven again and again, don’t low cost startups. Give them a expertise breakthrough, and entrepreneurs will discover a strategy to construct nice corporations.

Sure, when cell appeared, all corporations grew to become mobile-enabled. Nevertheless, founders constructed nice startups that would not have existed with out the cell platform shift – Uber being the obvious instance.

Who would be the Uber of generative AI?

The brand new era of AI Labs is probably constructing the AWS, somewhat than Uber, of generative AI. OpenAI, Anthropic, Stability AI, Adept, Midjourney and others are constructing broad horizontal platforms upon which many functions are already being created. It’s an costly enterprise, as constructing massive language fashions is extraordinarily useful resource intensive, though maybe prices are going to drop quickly. The enterprise mannequin of these platforms continues to be being labored out. OpenAI launched ChatGPT Plus, a paying premium model of ChatGPT. Stability AI plans on monetizing its platform by charging for customer-specific variations.

There’s been an explosion of latest startups leveraging GPT, particularly, for all kinds of generative duties, from creating code to advertising copy to movies. Many are derided as being a “skinny layer” on prime of GPT. There’s some reality to that, and their defensibility is unclear. However maybe that’s the improper query to ask. Maybe these corporations are simply the following era of software program somewhat than AI corporations. As they construct extra performance round issues like workflow and collaboration on prime of the core AI engine, they are going to be no extra, but additionally no much less, defensible than your common SaaS firm.

We consider that there are many alternatives to construct nice corporations: vertical-specific or task-specific corporations that may intelligently leverage generative AI for what it’s good at. AI-first corporations that may develop their very own fashions for duties that aren’t generative in nature. LLM-ops corporations that may present the required infrastructure. And so many extra.

This subsequent wave is simply getting began, and we are able to’t wait to see what occurs.

Matt Turck is a VC at FirstMark, the place he focuses on SaaS, cloud, information, ML/AI, and infrastructure investments. Matt additionally organizes Information Pushed NYC, the biggest information neighborhood within the U.S.

This story initially appeared on Mattturck.com. Copyright 2023

DataDecisionMakers

Welcome to the VentureBeat neighborhood!

DataDecisionMakers is the place consultants, together with the technical individuals doing information work, can share data-related insights and innovation.

If you wish to examine cutting-edge concepts and up-to-date data, greatest practices, and the way forward for information and information tech, be a part of us at DataDecisionMakers.

You may even take into account contributing an article of your personal!

{kind=link}

Наша группа квалифицированных исполнителей проштудирована предоставить вам актуальные подходы, которые не только гарантируют надежную безопасность от мороза, но и подарят вашему жилью элегантный вид.

Мы эксплуатируем с последовательными веществами, ассигнуруя долгосрочный период службы и прекрасные итоги. Изоляция внешнего слоя – это не только экономия тепла на подогреве, но и забота о природной среде. Энергоэффективные методы, которые мы применяем, способствуют не только дому, но и сохранению природных ресурсов.

Самое ключевое: [url=https://ppu-prof.ru/]Стоимость утепления дома снаружи цена[/url] у нас составляет всего от 1250 рублей за м2! Это бюджетное решение, которое сделает ваш помещение в подлинный тепличный район с скромными затратами.

Наши труды – это не лишь утепление, это образование помещения, в где каждый компонент отразит ваш свой образ действия. Мы учтем все твои требования, чтобы осуществить ваш дом еще больше уютным и привлекательным.

Подробнее на [url=https://ppu-prof.ru/]www.ppu-prof.ru[/url]

Не откладывайте труды о своем обители на потом! Обращайтесь к квалифицированным работникам, и мы сделаем ваш дворец не только уютнее, но и стильнее. Заинтересовались? Подробнее о наших работах вы можете узнать на интернет-портале. Добро пожаловать в пределы гармонии и стандартов.

Наша бригада искусных мастеров подготовлена предоставлять вам прогрессивные системы, которые не только гарантируют долговечную охрану от холодных воздействий, но и преподнесут вашему домашнему пространству изысканный вид.

Мы работаем с новыми материалами, заверяя долгий период использования и прекрасные результаты. Утепление фасада – это не только сбережение на отоплении, но и внимание о окружающей среде. Энергосберегающие технологии, какие мы применяем, способствуют не только твоему, но и сохранению природы.

Самое важное: [url=https://ppu-prof.ru/]Утепление здания снаружи цена[/url] у нас открывается всего от 1250 рублей за м²! Это доступное решение, которое превратит ваш помещение в истинный комфортный район с минимальными тратами.

Наши произведения – это не всего лишь изоляция, это формирование поля, в где каждый член символизирует ваш уникальный образ действия. Мы примем все ваши потребности, чтобы переделать ваш дом еще более гостеприимным и привлекательным.

Подробнее на [url=https://ppu-prof.ru/]веб-сайте[/url]

Не откладывайте заботу о своем ларце на потом! Обращайтесь к мастерам, и мы сделаем ваш жилище не только более теплым, но и стильнее. Заинтересовались? Подробнее о наших делах вы можете узнать на интернет-портале. Добро пожаловать в пространство спокойствия и качественного исполнения.

Наша бригада профессиональных мастеров находится в готовности предлагать вам прогрессивные системы утепления, которые не только подарят надежную защиту от заморозков, но и дарят вашему дому оригинальный вид.

Мы функционируем с современными материалами, заверяя долгий продолжительность эксплуатации и отличные результирующие показатели. Утепление фасада – это не только экономия на отапливании, но и заботливость о окружающей среде. Энергоэффективные технологии, какие мы применяем, способствуют не только жилищу, но и поддержанию природных ресурсов.

Самое важное: [url=https://ppu-prof.ru/]Стоимость утепления стен домов[/url] у нас стартует всего от 1250 рублей за квадратный метр! Это бюджетное решение, которое превратит ваш хаус в реальный комфортный корнер с скромными расходами.

Наши произведения – это не всего лишь изоляция, это составление пространства, в где каждый элемент преломляет ваш индивидуальный моду. Мы возьмем во внимание все ваши требования, чтобы осуществить ваш дом еще более теплым и привлекательным.

Подробнее на [url=https://ppu-prof.ru/]ppu-prof.ru/[/url]

Не откладывайте заботу о своем квартире на потом! Обращайтесь к исполнителям, и мы сделаем ваш корпус не только более теплым, но и стильным. Заинтересовались? Подробнее о наших услугах вы можете узнать на интернет-портале. Добро пожаловать в мир комфорта и качества.