The beneath is an excerpt from a latest version of Bitcoin Journal Professional, Bitcoin Journal’s premium markets publication. To be among the many first to obtain these insights and different on-chain bitcoin market evaluation straight to your inbox, subscribe now.

Hypothesis And Yields

This cycle has been tremendous charged by hypothesis and yield, main all the best way again to the preliminary Grayscale Bitcoin Belief premium arbitrage alternative. That chance out there incentivized hedge funds and buying and selling retailers from everywhere in the world to lever up with the intention to seize the premium unfold. It was a ripe time for being profitable, particularly again in early 2021 earlier than the commerce collapsed and switched to the numerous low cost we see in the present day.

The identical story existed within the perpetual futures market the place we noticed 7-day common annualized funding charges attain as much as 120% at peak. That is the implied annual yield that lengthy positions had been paying out there to quick positions. There have been an abundance of alternatives within the GBTC and futures markets alone for yield and fast returns available — with out even mentioning the bucket of DeFi, staking tokens, failed initiatives and Ponzi schemes that had been producing even larger yield alternatives in 2020 and 2021.

There’s an ongoing, vicious suggestions loop the place larger costs drive extra hypothesis and leverage, which, in flip, drive larger yields. Now, we’re coping with this cycle in reverse. Decrease costs wipe out extra hypothesis and leverage whereas washing out any “yield” alternatives. Because of this, yields in every single place have collapsed.

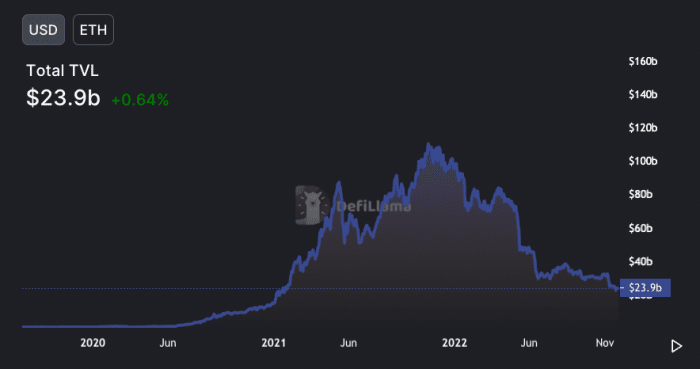

“Complete worth locked” within the Ethereum DeFi ecosystem surpassed over $100 billion in 2021 throughout the speculative mania, and is now a mere $23.9 billion in the present day. This leverage-fueled mania within the crypto ecosystem fueled the expansion of the “yield” merchandise provided by the market, most of which have all collapsed now that the figurative tide has drawn out.

The full worth locked in Ethereum DeFi ecosystem has largely disappeared

This dynamic introduced concerning the rise of bitcoin and cryptocurrency yield-generating merchandise, from Celsius to BlockFi to FTX and lots of extra. Funds and merchants seize a juicy unfold whereas kicking again a few of these earnings to the retail customers who hold their cash on exchanges to get a small quantity of curiosity and yield. Retail customers know little about the place the yield comes from or the dangers concerned. Now, all of these short-term alternatives out there appear to have evaporated.

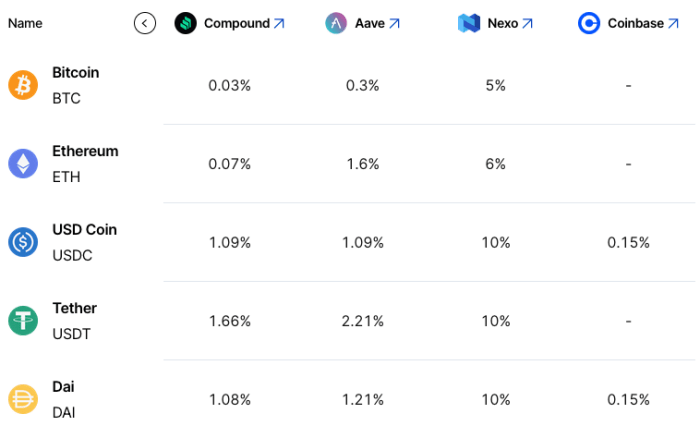

With the entire speculative trades and yield gone, how can firms nonetheless provide such high-yielding charges which are properly above conventional “risk-free” charges out there? The place does the yield come from? To not single out or FUD any particular firms, however take Nexo for instance. Charges for USDC and USDT are nonetheless at 10% versus 1% on different DeFi platforms. The identical goes for bitcoin and ethereum charges, 5% and 6% respectively, whereas different charges are largely nonexistent elsewhere.

These excessive borrow charges are collateralized with bitcoin and ether providing a 50% LTV (loan-to-value ratio) whereas quite a lot of different speculative tokens can be utilized as collateral as properly at a a lot decrease LTV. Nexo shared an in depth thread on their enterprise operations and mannequin. As we’ve discovered time and time once more, we are able to by no means know for certain which establishments to belief or to not belief as this trade de-leveraging continues. Nonetheless, the primary inquiries to ask are:

- Will a 13.9% mortgage demand be a sustainable enterprise mannequin going ahead into this bear market? Gained’t charges have to come back down additional?

- No matter Nexo’s threat administration practices, are there heightened counterparty dangers at present for holding buyer balances on quite a few exchanges and DeFi protocols?

Charges on totally different DeFi lending platforms

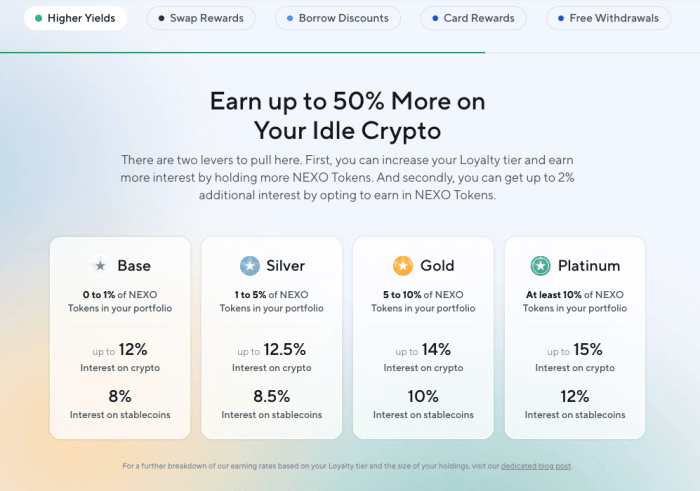

Present charges on Nexo’s yield-generating choices

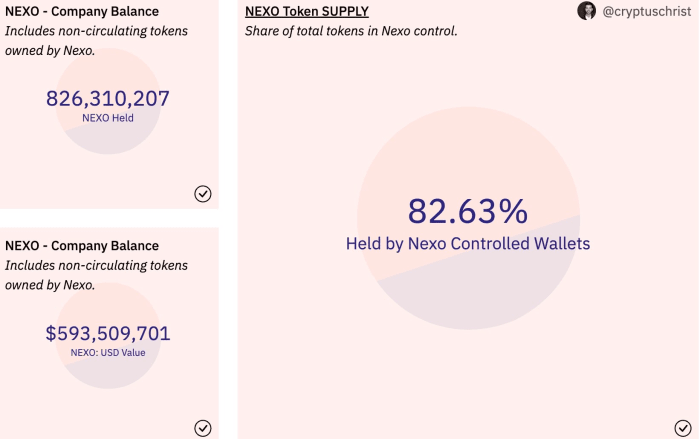

Statistics for Nexo’s firm holdings

Here’s what we all know:

The crypto-native credit score impulse — a metric that’s not completely quantifiable however imperfectly observable through a wide range of datasets and market metrics — has plunged from its 2021 euphoric highs and now seems to be extraordinarily detrimental. Which means any remaining product that’s providing you crypto-native “yield” is more likely to be underneath excessive duress, because the arbitrage methods that fueled the explosion in yield merchandise all through the bull market cycle have all disappeared.

What stays, and what’s going to emerge from the depths of this bear market would be the belongings/initiatives constructed on the strongest of foundations. In our view, there’s bitcoin, and there’s all the things else.

Readers ought to consider counterparty threat in all types, and keep away from any of the remaining yield merchandise that exist out there.

Related Previous Articles:

{kind=link}